Dark Mode

Aspect based Sentiment Analysis for Financial News

Data Science and Analytics

Tags and Keywords

Trusted By

"No reviews yet"

Free

About

Fine-grained financial sentiment analysis on news headlines is a challenging task requiring human-annotated datasets to achieve high performance. Limited studies have tried to address the sentiment extraction task in a setting where multiple entities are present in a news headline. In an effort to further research in this area, we make publicly available SEntFiN 1.0, a human-annotated dataset of 10,700+ news headlines with entity-sentiment annotations, of which 2,800+ headlines contain multiple entities, often with conflicting sentiments.

Acknowledgements

Sinha, A., Kedas, S., Kumar, R., & Malo, P. (2022). SEntFiN 1.0: Entity‐aware sentiment analysis for financial news. Journal of the Association for Information Science and Technology.

DOI: https://doi.org/10.1002/asi.24634

Please refer to the above paper for further details about dataset creation and analysis. We propose a framework that enables the extraction of entity-relevant sentiments using a feature-based approach rather than an expression-based approach. For sentiment extraction, we utilize 12 different learning schemes utilizing lexicon-based and pretrained sentence representations and five classification approaches. Our experiments indicate that overall, RoBERTa was the best performer with other BERT-based models as close competitors.

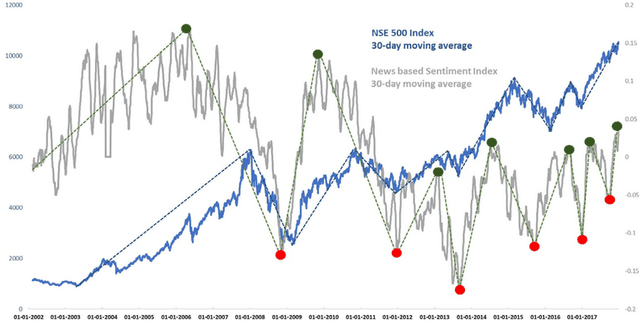

In our study, we have also validated the effect of news sentiments on aggregate market movements.

Original Data Source: Aspect based Sentiment Analysis for Financial News